Detailed Summary of Recommendations from the 54th GST Council Meeting

Services

Business Incorporation & Compliance

Registration & Certification Services

GST Advisory & Compliance

Income Tax Advisory & Compliance

Accounting and Payroll Services

Audit & Assurance Services

International Tax Services

UAE Business Services

Financial Insights

Detailed Summary of CBIC Instruction No. 03/2025-GST

Union Budget 2025: Goods and Services Tax Comprehensive Overview

Union Budget 2025: Direct Tax Comprehensive Overview

Detailed Summary of Recommendations from the 54th GST Council Meeting

Union Budget 2025: Goods and Services Tax Comprehensive Overview

Detailed Summary of Recommendations from the 54th GST Council Meeting

Date: 9th September 2024

Chairperson: Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman

Attendees: Union Minister of State for Finance Shri Pankaj Chaudhary, Chief Ministers of Goa and Meghalaya, Deputy Chief Ministers of Arunachal Pradesh, Bihar, Madhya Pradesh, and Telangana, Finance Ministers of States & UTs (with legislature), and senior officers of the Ministry of Finance & States/UTs.

Key Recommendations by GST Council

- Formation of Groups of Ministers (GoMs):

- GoM on Life and Health Insurance: A new GoM will be established to address GST issues concerning life and health insurance. This GoM will work alongside the existing GoM on Rate Rationalisation and is tasked with submitting its report by the end of October 2024. The GoM will include representatives from Bihar, Uttar Pradesh, West Bengal, Karnataka, Kerala, Rajasthan, Andhra Pradesh, Meghalaya, Goa, Telangana, Tamil Nadu, Punjab, and Gujarat.

- GoM on Compensation Cess: Another GoM will be set up to examine the future of the compensation cess, focusing on its continuation and implications.

- Changes in GST Tax Rates Related to Goods:

- Cancer Drugs: The GST rate on specific cancer drugs, namely Trastuzumab Deruxtecan, Osimertinib, and Durvalumab, will be reduced from 12% to 5%. This reduction aims to make cancer treatment more affordable.

- Namkeens and Savoury Food Products: The GST rate for extruded or expanded savoury food products, such as those classified under HS 1905 90 30, will be reduced from 18% to 12%. This change aligns these products with the GST rate for similar ready-to-eat items like namkeens and bhujia. The 5% GST rate will continue for un-fried or un-cooked snack pellets.

- Metal Scrap: A Reverse Charge Mechanism (RCM) will be introduced for metal scrap supplied by unregistered persons to registered persons. Registered persons will need to pay the tax, even if the supplier is below the threshold limit. Additionally, a 2% Tax Deducted at Source (TDS) will be applicable on metal scrap supplied by registered persons in B2B transactions.

- Roof Mounted Package Unit (RMPU) Air Conditioning Machines: These units, used in railway applications, will be classified under HSN 8415 and attract a GST rate of 28%.

- Car and Motorcycle Seats: The GST rate on car seats classified under HSN 9401 will increase from 18% to 28%, aligning it with the rate for motorcycle seats.

- Changes in GST Tax Rates Related to Services:

- Research and Development Services: The GST Council has recommended exempting research and development services provided by government entities, research associations, universities, colleges, or institutions notified under section 35 of the Income Tax Act, when using government or private grants. Past GST demands related to these services will be regularized on an ‘as is where is’ basis.

- Transport by Helicopters: GST on passenger transport by helicopters on a seat-share basis will be set at 5%. The GST for charter helicopter services will remain at 18%. Past GST demands for helicopter transport services will also be regularized.

- Flying Training Courses: Approved flying training courses conducted by DGCA-approved Flying Training Organizations will be exempt from GST. This exemption aims to support the aviation training sector.

- Affiliation Services: Affiliation services provided by educational boards like CBSE will be taxable. However, affiliation services to government schools provided by State/Central educational boards and similar bodies will be exempt from GST prospectively. Issues related to past periods (01.07.2017 to 17.06.2021) will be addressed on an ‘as is where is’ basis.

- Import of Services by Branch Offices: The import of services by foreign airline branch offices from related entities or establishments outside India, when made without consideration, will be exempt from GST. Past periods will be regularized on the same basis.

- Trade Facilitation and Compliance Measures:

- Waiver of Interest/Penalty: The GST Council recommended the insertion of Rule 164 in CGST Rules, 2017, detailing the procedure and conditions for waiving interest or penalties for tax demands from FYs 2017-18, 2018-19, and 2019-20. Registered persons must pay the tax by 31st March 2025 to avail of this benefit. The Council will also issue a circular to clarify the process and conditions for availing the waiver.

- Amendments in CGST Rules: The Council recommended the notification of Section 118 and 150 of the Finance (No. 2) Act, 2024, which introduces new provisions in Section 16 of the CGST Act, 2017, retrospectively from 01.07.2017. A special procedure for rectifying orders related to wrong availment of input tax credit will also be introduced, along with a circular to address related issues.

- IGST Refunds on Exports: The Council recommended clarifications regarding IGST refunds on exports when inputs were initially imported under concessional notifications but subsequently paid with IGST and compensation cess. To simplify the refund process, rules 96(10), 89(4A), and 89(4B) of CGST Rules, 2017, will be prospectively omitted.

- Clarifications and Circulars: Issuance of circulars to address ambiguities and disputes on various issues, including:

- Place of Supply of advertising services provided by Indian companies to foreign entities.

- Availability of Input Tax Credit on demo vehicles.

- Place of Supply of data hosting services provided to foreign cloud computing service providers.

- Other Measures:

- B2C E-Invoicing: A pilot program for B2C e-Invoicing will be rolled out, following successful implementation in the B2B sector. This initiative aims to enhance business efficiency, reduce errors, and allow retail customers to verify invoice reporting. The pilot will be voluntary and implemented in select sectors and states.

- Invoice Management System (IMS): Enhancements to the GST return architecture include the introduction of a Reverse Charge Mechanism (RCM) ledger, an Input Tax Credit Reclaim ledger, and an Invoice Management System (IMS). Taxpayers can declare their opening balances for these ledgers by 31st October 2024. The IMS will help taxpayers manage invoice acceptance, rejection, or pending status, aiming to improve accuracy and reduce ITC mismatch notices.

The recommendations from this GST Council meeting seek to streamline tax administration, provide targeted relief, and improve compliance and trade facilitation. These changes will be implemented through relevant circulars, notifications, and amendments to existing laws.

Read More Insights

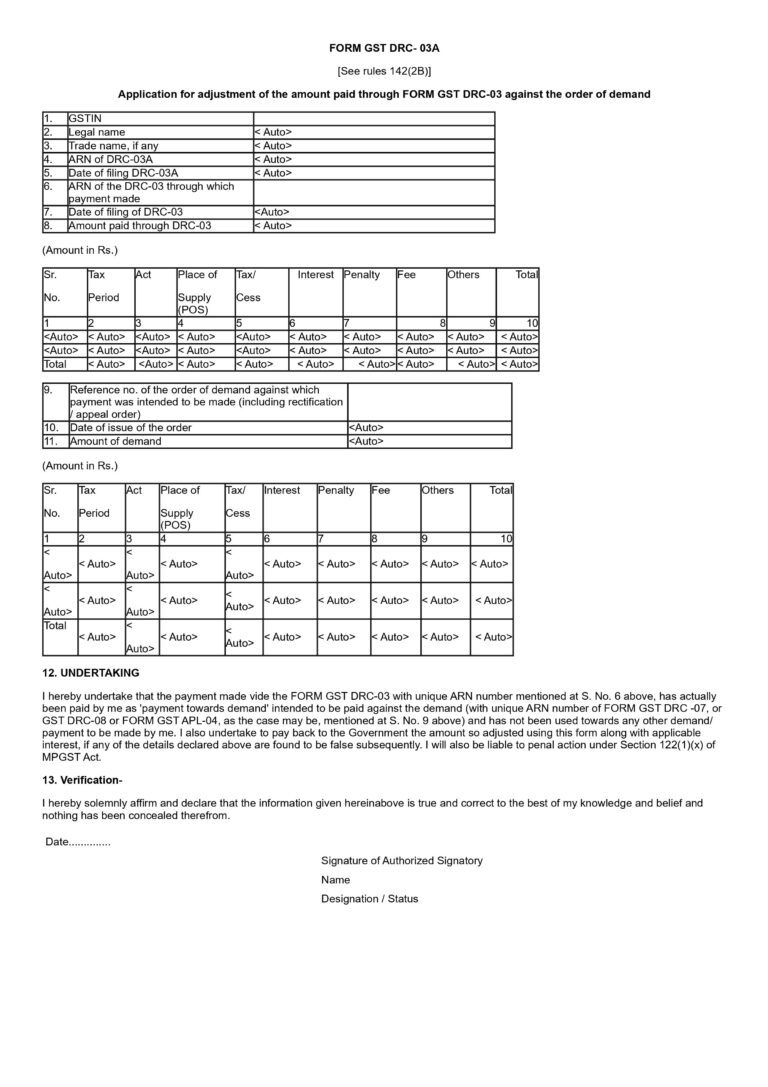

Clarification on GST Payments Through Form GST DRC-03 and Introduction of Form GST DRC-03A

Clarification on GST Payments Through Form GST DRC-03 and Introduction of Form GST DRC-03A Home Insights Clarification on GST Payments Through Form GST DRC-03 and

Standard Chartered Bank vs. The Principal Commissioner Of Central Tax & Others – Telangana High Court Judgment (11 July 2024)

Standard Chartered Bank vs. The Principal Commissioner Of Central Tax & Others – Telangana High Court Judgment (11 July 2024) Home Insights Standard Chartered Bank

Union Budget 2025: Goods and Services Tax Comprehensive Overview

Union Budget 2025: Goods and Services Tax Comprehensive Overview Home Insights Union Budget 2025: Goods and Services Tax Comprehensive Overview Services Business Incorporation & Compliance